One of the biggest private life insurance providers in India is Reliance Nippon Life Insurance. Reliance Nippon provides a wide choice of life insurance products that act as a shield for your loved ones, guaranteeing their future security and protection from life’s unforeseen events. Let’s learn more about Reliance Nippon Life Insurance Agent Commission Chart 2026.

What Is Reliance Nippon Life Insurance?

Table of Contents

One of the top insurance providers in the Indian private sector is Reliance Nippon Life Insurance. To assist people and families in safeguarding their financial future in the face of life’s uncertainties, it provides a range of insurance products, including Protection, Savings & Investments, Retirement, ULIP, NRI term Insurance, and Child Plans. Reliance Nippon life insurance plan premiums are available online.

How to Become a Reliance Nippon Life Insurance Agent?

To become a Reliance Nippon Life Insurance agent, here’s a step-by-step guide:

Eligibility:

Age:

Minimum of 18 years.

Education:

Urban areas: Completion of 12th standard or equivalent.

Rural areas: Completion of 10th standard or equivalent.

Contact Reliance Nippon Life Insurance:

- Visit their official website: reliancenipponlife.com

- Go to the “Become an Advisor” section.

- Fill out the application form with your personal and educational details.

Training:

- Attend 50 hours of mandatory training approved by the Insurance Regulatory and Development Authority of India (IRDAI).

- Training covers insurance sales, service, and marketing knowledge.

Pass the IRDAI Exam:

After training, you’ll need to pass the IRDAI licensing exam to become a certified insurance agent.

Get Licensed:

Once you pass the exam, you’ll receive your IRDAI license, officially allowing you to sell insurance products.

Start Selling:

With your license, you can start offering Reliance Nippon Life Insurance’s range of products and earn commissions on each policy you sell.

Benefit from Support and Growth:

Reliance Nippon provides ongoing training, marketing support, and opportunities for career growth.

You can work flexible hours and build long-term income.

Salary Of Reliance Nippon Life Insurance Agent:

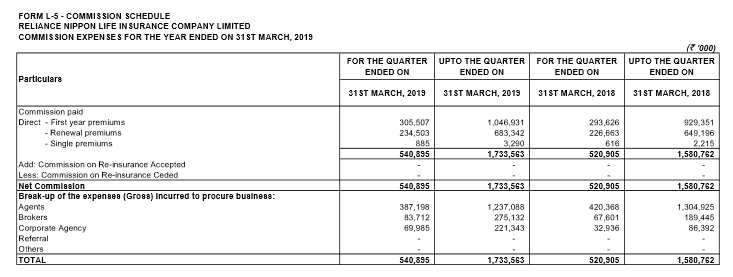

Reliance Nippon Life Insurance Agent Commission Chart 2026:

As of February 2026, specific details about the commission structure for Reliance Nippon Life Insurance agents have not been publicly disclosed. However, based on available information and industry standards, the following table provides an estimated overview of the Reliance Nippon life insurance agent commission:

| Policy Type | Commission Details |

|---|---|

| First-Year Premiums | Agents typically receive a significant commission on the first-year premium of a new policy, ranging between 60% to 80% of the premium amount. |

| Renewal Premiums | For premiums paid in subsequent years, agents usually earn a lower commission, often between 5% to 10% of the premium. |

| Single Premium Policies | These policies involve a one-time lump sum payment, and the agent’s commission is typically a smaller percentage of this amount. |

See here the Reliance Nippon Life Insurance Agent Commission Chart 2026 in PDF format.

Factors Affecting Reliance Nippon Life Insurance Agent Commission:

The commission earned by a Reliance Nippon Life Insurance agent depends on several factors. Let’s break down the key ones:

Type of Policy:

- Traditional Plans (Endowment, Whole Life): Usually offer higher commission rates.

- Term Insurance: Lower premiums, so commissions tend to be lower.

- Unit-Linked Insurance Plans (ULIPs): Commission rates can vary based on fund management charges and policy terms.

- Single-Premium Policies: Offer a one-time, lower commission percentage compared to regular premium policies.

Policy Term:

- Longer-term policies often offer higher first-year commissions and sustained renewal commissions.

- Short-term policies generally pay lower commissions due to limited premium-paying years.

Premium Amount:

- Higher premiums mean higher absolute commission earnings, even if the percentage remains the same.

Year of the Policy:

- First-Year Commission: Typically the highest, often 20% to 35% depending on policy type.

- Renewal Commission: Drops significantly, usually around 5% to 10% from the second year onward.

Agent’s Performance and Tenure:

- High-performing agents or those with a strong track record may qualify for bonuses or higher commission slabs.

- Senior agents with consistent sales might also earn loyalty incentives.

Persistency Ratio:

- Agents are rewarded when policyholders continue their policies without lapsing. Higher persistence leads to better long-term income and possibly bonus commissions.

Product Promotions:

- Special sales drives or newly launched products may offer additional incentives or higher commission rates for a limited period.

Geographical Location:

- Reliance Insurance agent commission structures can vary slightly between urban and rural markets based on policy demand and market conditions.

Agent Category:

- Full-time advisors might earn higher commissions and incentives compared to part-time or occasional agents.

Benefits of Becoming an ICICI Prudential Life Insurance Agent:

Becoming a Reliance Nippon Life Insurance agent comes with a lot of benefits — both financial and professional. Here’s a quick look:

Attractive Commission Structure:

Earn commissions on every policy sold, with high first-year commissions and renewal commissions for ongoing income.

Potential for performance-based incentives and bonuses.

Flexible Working Hours:

Work at your own pace and manage your schedule independently.

Perfect for people looking for part-time or full-time opportunities.

Unlimited Earning Potential:

Your income depends on your effort and the number of policies you sell.

Consistent performance can lead to significant long-term earnings.

Training and Skill Development:

Get professional training in insurance, sales, and financial advisory services.

Stay updated with market trends and enhance your communication and management skills.

Career Growth Opportunities:

Start as an agent and move up to higher roles like Sales Manager or Development Officer.

Get recognized for your achievements with awards and incentives.

Support from the Company:

Access marketing materials, digital tools, and guidance from experienced mentors.

Benefit from company-led promotional campaigns to attract potential clients.

Work-Life Balance:

Choose your work hours and maintain a balance between personal and professional life.

Freedom to work from home or meet clients at your convenience.

Social Impact:

Help people secure their future and provide financial protection for their families.

Build strong, long-term client relationships and earn their trust and respect.

Recognition and Rewards:

High-performing agents receive recognition through awards, international trips, and exclusive events.

Job Security and Independence:

As an agent, you’re an independent advisor without a fixed salary cap.

No upper limit on earnings and no risk of job loss due to company restructuring.

How to Calculate ICICI Prudential Life Insurance Agent Commission?

Calculating a Reliance Nippon Life Insurance agent’s commission involves understanding the commission structure, which varies based on policy type, premium amount, and policy term. Let’s break it down step by step:

Identify Policy Type:

Different policies offer different commission rates:

Traditional Plans (Endowment, Whole Life): Higher commission rates.

Term Insurance: Lower premiums, hence lower commission percentages.

ULIPs: Commission depends on fund management charges and policy duration.

Single-Premium Policies: One-time commission on a lump-sum premium.

Determine the Premium Amount:

The agent’s commission is always a percentage of the premium paid by the policyholder. Let’s call this the Annual Premium (AP).

Apply Commission Rate:

Reliance Nippon Life Insurance commission rates generally follow this pattern (estimated):

First-Year Premium: 20% to 35% of the annual premium.

Second-Year Premium: 5% to 7.5% of the annual premium.

Subsequent Years: 3% to 5% of the annual premium.

Calculate Commission:

Formula:

Commission = Premium Amount × Applicable Commission Rate

Example Calculation:

Let’s say an agent sells an endowment policy with an annual premium of ₹50,000 and a 20-year term:

- First-Year Commission: ₹50,000 × 30% = ₹15,000

- Second-Year Commission: ₹50,000 × 7.5% = ₹3,750

- Third-Year Onwards: ₹50,000 × 5% = ₹2,500 (annually)

Add Bonuses or Incentives (If Applicable):

Reliance Nippon often offers performance-based incentives, contest rewards, and bonuses for high-performing agents. These can add to the total earnings.

Factor in Renewal Commission:

Commissions aren’t limited to the first year agents earn renewal commissions as long as the policy remains active and premiums are paid.

FAQs:

Q. What is the commission structure for Reliance Nippon Life Insurance agents?

A. The commission depends on the type of policy and its term:

First-Year Premium: 20% to 35% commission (varies by policy type).

Renewal Premiums (2nd Year Onwards): 5% to 7.5% commission.

Subsequent Years: 3% to 5% of annual premium.

Single-Premium Policies: One-time, lower percentage commission.

Q. How is an agent’s commission calculated?

A. The formula:

Commission=Premium Amount×Commission RateCommission=Premium Amount×Commission Rate

For example, if the annual premium is ₹50,000 and the first-year commission rate is 30%:

₹50,000×30%=₹15,000₹50,000×30%=₹15,000

Q. Do agents earn commissions on policy renewals?

A. Yes! Agents receive renewal commissions for as long as the policyholder pays premiums – typically 5% to 7.5% for the second year and around 3% to 5% from the third year onward.

Q. Are there additional bonuses or incentives?

A. Yes! Reliance Nippon Life Insurance often provides performance-based incentives, contests, and recognition awards for high-performing agents.

Q. Is there a difference in commission based on policy type?

A. Yes, commission rates vary by product:

Traditional Plans (Endowment, Whole Life): Higher commission rates.

Term Plans: Lower commission due to lower premium amounts.

ULIPs: Varying commissions based on fund charges and policy terms.

Q. How long does an agent earn commissions on a policy?

A. As long as the policy remains active and the policyholder pays the premium, the agent continues earning renewal commissions.

Q. Do agents get commissions on single-premium policies?

A. Yes, but the rate is lower and applies only to the one-time premium paid.

Q. Can an agent’s commission increase over time?

A. Yes, based on performance, persistency ratio (renewal rate of policies), and achievement of sales targets, agents can qualify for higher commission slabs and bonuses.

Q. What is the persistency ratio, and how does it affect commissions?

A. The persistency ratio measures how many policies remain active over time. A higher ratio means more renewal commissions and potential bonus incentives.

Q. Is there a cap on how much commission an agent can earn?

A. No! Your earning potential is unlimited. The more policies you sell and retain, the more you earn.