As we move through 2026, the insurance industry continues to evolve with new products, digital tools, and compensation models. For life insurance agents, especially those specializing in universal life (UL) insurance, understanding the current commission structure is critical to optimizing income and long-term success. The Universal Life Insurance Agent Commission Chart 2026 outlines the earnings agents can expect from various UL policy types, including traditional UL, indexed UL, and variable UL. This comprehensive guide explores commission rates, influencing factors, market trends, and actionable tips to help agents boost their revenue in a competitive environment.

What is the Universal Life Insurance Agent Commission Chart 2026?

Table of Contents

The Universal Life Insurance Agent Commission Chart 2026 refers to the updated commission structure insurance agents receive for selling universal life (UL) insurance policies in the year 2026. Universal life insurance is a type of permanent life insurance that combines life coverage with an investment savings element. Commissions are a major source of income for agents, and these rates are typically paid as a percentage of the first-year premium and, sometimes, the policy’s renewal premiums.

As the insurance market continues to evolve, understanding the 2026 commission chart helps agents stay competitive and maximize their earning potential.

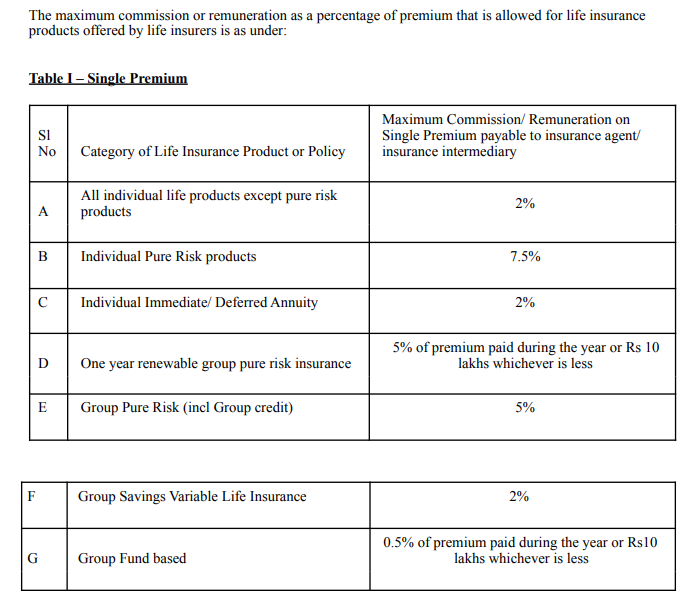

Universal Life Insurance Agent Commission Chart 2026:

Below is a general overview of what the 2026 commission structure looks like for agents selling universal life insurance policies (note that these numbers may vary slightly by company):

| Commission Type | Percentage of Premium | Notes |

|---|---|---|

| First-Year Commission | 50% – 90% | Highest earnings vary by experience level |

| Renewal Commissions (Years 2-5) | 2% – 5% | Paid annually during the early policy years |

| Trail Commissions (After Year 5) | 1% – 2% | Ongoing income for policy maintenance |

| Bonus or Incentives | 5% – 15% | For high-volume or top-performing agents |

Some carriers also offer persistency bonuses and performance-based incentives, such as luxury trips or additional commissions for reaching sales milestones.

Types of Universal Life Insurance:

Universal life insurance comes in various forms, each of which may affect commission rates:

Traditional Universal Life (UL):

- Flexible premiums and adjustable death benefits.

- Moderate commission levels.

Indexed Universal Life (IUL):

- Cash value grows based on a market index (e.g., S&P 500).

- Typically offers higher commissions due to complexity and popularity.

Variable Universal Life (VUL):

- Offers investment options for the policy’s cash value.

- Agents may need a securities license and may earn trail commissions based on assets under management.

Guaranteed Universal Life (GUL):

- Focused on long-term, fixed death benefit with minimal cash value.

- Often lower commission compared to IUL or VUL.

Factors Influencing Universal Life Insurance Agent Commission:

Several key factors impact how much an agent earns from selling UL insurance in 2026:

- Insurance Carrier Policy: Each company sets its own commission structures.

- Agent Experience Level: New agents often receive lower rates than seasoned professionals or broker-dealers.

- Policy Size and Premium: Larger policies and higher premiums yield higher commissions.

- Product Type: As noted, IUL and VUL policies typically carry higher commissions.

- Distribution Channel: Independent agents, captive agents, and brokers may earn differently.

- Licensing and Certifications: Having FINRA registration for selling VUL products can increase earning potential.

Market Trends Impacting Agent Earnings

Several industry trends are shaping the commission landscape in 2026:

- Shift Toward Fee-Based Advice: There’s a growing trend toward advisory models and reduced dependency on commissions alone.

- Technology Integration: Tools like AI-based underwriting and digital platforms streamline processes, enabling more sales in less time.

- Regulatory Changes: Enhanced transparency rules in commissions may affect compensation disclosure and structures.

- Focus on Client Education: Agents investing in client financial literacy often see higher policy persistency, boosting renewal commissions.

How to Maximize Universal Life Insurance Agent Commission in 2026:

- Sell High-Premium IUL/VUL Policies: These often offer the best compensation packages.

- Upskill Regularly: Gain certifications (like CLU or securities licenses) to sell a broader range of products.

- Focus on Retention: Build relationships and provide service to retain clients and secure renewal and trail commissions.

- Use Digital Tools: Automate lead generation, CRM, and quoting tools to scale sales efforts.

- Partner with Top Carriers: Align with insurance companies offering the most competitive commission rates and incentives.

- Participate in Incentive Programs: Aim for bonuses and recognition-based commissions through volume and consistency.

Conclusion:

The Universal Life Insurance Agent Commission Chart 2026 reflects a dynamic earning structure that rewards performance, product knowledge, and client service. While first-year commissions remain a lucrative component, long-term income through renewals and trails depends on maintaining strong client relationships and adapting to changing market conditions. As demand for UL policies continues to rise, agents equipped with current knowledge and tools are best positioned to thrive.

FAQs:

Q. How much can an agent earn from selling a single universal life insurance policy in 2026?

A: Depending on the policy size and commission rate, an agent may earn anywhere from $500 to over $10,000 on a single policy.

Q. Which type of universal life policy offers the highest commission?

A: Indexed Universal Life (IUL) policies typically offer the highest commissions due to their complexity and client demand.

Q. Are renewal commissions guaranteed for all universal life policies?

A: Not always. Renewal and trial commissions depend on the carrier’s policies and whether the client maintains the policy.

Q. Can agents earn bonuses on top of standard commissions?

A: Yes, many carriers offer performance bonuses, persistency rewards, and incentive trips.

Q. Is it better to be a captive or an independent agent for higher commissions?

A: Independent agents often have access to multiple carriers and higher commissions but may lack the support and benefits offered to captive agents.