Are searching for you quarries regarding what is ULIP Insurance plan and whether you should take a ULIP insurance plan or not and what is the difference between ULIP and mutual funds etc.? If your answer is “YES” then you have come to the right place as today I am going discuss what is ULIP Insurance plan and how it works and so many more.

If you want to invest for the short term, then it is better to invest in mutual funds with the help of a consultant. But if you want to invest for the long term then the ULIP insurance plan is best suited for you. To know more about insurance and other aspects, read our article on Insurance in detail.

What Is ULIP Insurance Plan?

Table of Contents

Unit Linked Insurance Plan (ULIP) is an option by which you can invest in life insurance and mutual funds simultaneously. Unit Linked Insurance (ULIP) can go for a combination of insurance and investment. Here the policyholder can pay monthly or annual premiums. That’s what is ULIP Plan

A small portion of the premium secures life insurance and the rest of the money is invested in mutual funds. Policyholder invests up to 5, 10 or 15 according to the policy term, and deposits the units. ULIP offers a good investment option for those who want to invest in equity or debt. That’s what is unit linked insurance plan

Nowadays ULIP (Unit-Linked Insurance Plan) is a preferred term for those who invest in the longer-term. There are also reasonable reasons for this. ULIP is a very good way of investing if you want to stay invested for a long period of time i.e. for 10 to 20 years. cSo, now you know what is ULIP insurance plan. Let’s now know other details besides what is ULIP insurance plan

What Is The Difference Between ULIP Insurance Plan And Mutual Funds?

The main difference between the ULIP insurance plan and Mutual Funds is the structure of charges. In ULIP insurance, a part of your premium is deducted for the overcharge of the insurance plan. Investment in the ULIP insurance plan may be better, due to a lack of surcharges. The FMC fund management charge is usually 1.5% (in any company, it is reduced to 0.8%) in ULIP, whereas in Mutual funds usually, the FMC is around 2.5%.

That is why, in the long run, when your fund becomes very large, the difference of 1% is also very important. In ULIP, you will also get life insurance plans, plan for children, and pension plans. You can also start with a minimum investment of Rs.1500 / – per month. Most companies also provide ECS facility. That what is ULIP insurance plan provide

How Does The ULIP Insurance Plan Works?

Now as you already know what ULIP insurance plan you might be wondering how is the ULIP insurance plan work. Well, ULIP (Unit Linked Insurance Plan) is a combination of insurance and investment.

When you pay a premium, one part of it is used by the insurance company to provide you insurance coverage and the rest are used to invest in debt and equity securities.

NOTE:

The assessment to withdraw your ULIP plan becomes difficult when you lose the insurance cover.

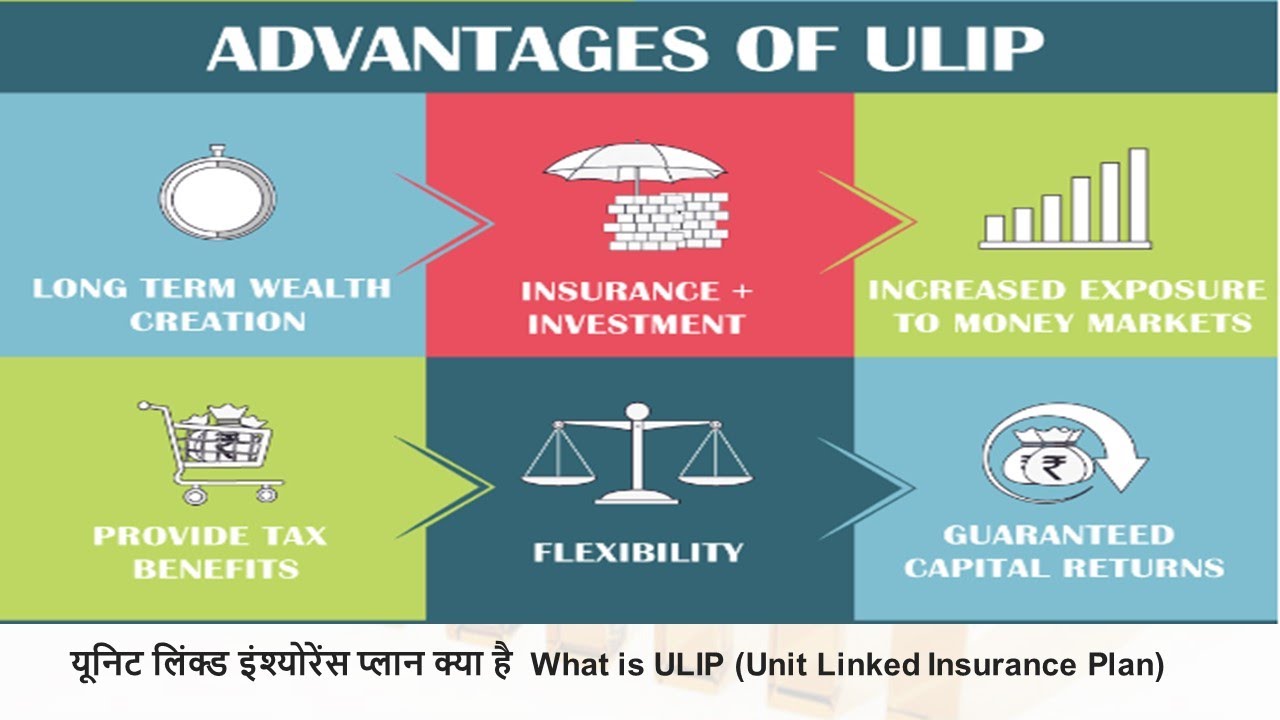

What Is ULIP Insurance Plan Benefits?

If you are searching for what is ULIP insurance benefits then let me tell you that just like other insurance plans in India ULIP insurance plans to has some of the outstanding benefits. Let’ now check out the what is ULIP insurance benefits in details:

Life Safety Investment and Savings

Unit Linked Insurance Plan (ULIP) provides two benefits of life insurance and savings in returns related to the market. Thus, keeping in mind your security needs, there is an opportunity to invest your money to earn higher returns. Unit-linked schemes help in the regular habit of investment, which is important for building wealth during long periods.

Long Term Savings:

ULIP (Unit Linked Insurance Plan) is usually extended for a tenure of 5 years or more. Just like other insurance plans, long-term commitments are required to pay the premium, for which the policy will be well paid when mature.

Market-linked returns

The unit-linked insurance plan (ULIP) insurance plan gives you the opportunity to earn market-related returns as a part of the premium invested in the funds linked to the market, which invests in different market instruments. This return includes different proportions in debt instruments and equity.

NOTE:

Since ULIPs are invested in the fund, market-linked instruments, so if the market is in your favor then you get an opportunity to get extraordinary returns.

Tax Benefits:

Profit from ULIP (Unit Linked Insurance Plan) is tax-free under Section 80C and Section 10D.

Upon the death of the policyholder, due to the maturity of the policy or the partial withdrawal of the policyholder’s will, the return of ULIP will be returned.

Partial Withdrawal:

If the refund is not greater than 20% of the fund value of the policy and the lock-in period is created after the expiry, then you will get a tax-free facility from the insurance company.

Maturity Benefits:

The policyholder gets the maturity benefit under the ULIP insurance plan under Section 10D of the Income Tax Act.

Death Benefit:

The return on the death of the policyholder is tax-free completely

Recommended Articles :-

- Mobile Insurance India: Know What Are The Top Companies

- Insurance Institute Of India: Get A Brief Idea About It

- Times Global Insurance: Protect Your Mobile, Laptop & iPhone

- Know In Details About National Insurance Parivar Mediclaim

- Retirement Life Insurance Benefits: What These Plans Cover

- Retirement Life Insurance Plans In India: Know In Details

Premium Payment:

You can make a claim for a tax rebate on the premium paid on the ULIP insurance, which has been invested in debt, money market, or equity instruments under Section 80C. For the present and the coming year, the limit of Section 80C is INR 1.5 lakhs.

Premium Extra:

In the later phase, additional premiums offered in the scheme are tax-exempt under section 80C and 10D, if it is not more than 10% of the sum insured.

Flexibility

Unit Linked Insurance Plan (ULIP) provides you with a wide range of flexible options, such as the option to switch between the investment fund according to your changing needs, partly due to the fees and conditions and partly back from your fund, convenience, etc.

So, basically, the ULIP insurance plan gives you the option to switch between different investment plans, according to your needs.

Single-Premium Facility:

You can also create a single premium edition to increase your investment in your ULIP insurance plan. Single-Premium means a lump sum payment.

NOTE:

Premium Plan You can pay a lump sum in the form of premium alone or you can opt for periodic payments based on your plan for a fixed period of years.

What Is ULIP Insurance Charges?

ULIP (Unit Linked Insurance Plan) is an outstanding investment option and it is very important to carefully understand these ULIP insurance charges before you make any investment in the ULIP insurance plan.

What Is ULIP Insurance Premium allocation Charges?

These kinds of charges are straightaway deducted from your premium. The remaining sum is used for the investment in your funds. According to the insurance corporations, these charges lookout for their distributor charges and the fees.

Charges for the premium allocation are generally high only for the duration of the first few years of your investment.

What Is ULIP Insurance Fund Management Charges?

These types of charges are imposed towards handling the funds, & thus are indicted as a percent of your assets’ worth. Charges for the Fund Management are higher for equity-oriented funds as compared to the debt-oriented funds.

What Is ULIP Insurance Policy Administration Charges?

The policy administration charges are subtracted towards the administrative costs, which the insurance corporation acquire to maintain your insurance policy. These administrative costs are including the paperwork charge or costs for timely reminders sending to its policyholder regarding the premium’s due date and so on.

Usually, depending on the policy, these policy administration charges are subtracted each month. These administration charges may stay the same during the course of the term of your policy or it can also increase at rates approved at the early stage.

What Is ULIP Insurance Mortality Charges?

Mortality Charges are associated with ULIP insurance components. These charges are typically charged once each month. The charges for mortality depend on various factors such as the age of the policyholder, the total sum of coverage, policyholder’s health status, and so many more.

What Is ULIP Insurance Surrender charge?

These Surrender Charges are basically for encashment of either full or partial units, before their identified end date. The Insurance Regulatory and Development Authority of India (IRDAI) has set a cap on its maximum surrender charges by the insurance corporations to be charged.

The discontinuance or surrender charges that are imposed differ in relation to when the policyholder surrenders the insurance policy & how much premiums you pay, although it can’t exceed INR 6000/-. If you surrender your ULIP insurance after completion of 5 years of the insurance plan i.e. once the policy’s lock-in period is completely over, then you don’t have to pay surrender charges.

Different Types Of ULIP Insurance Plan:

There are many companies in India that provide you different ULIP plans. Let’s now talk about what is a ULIP insurance plan type.

What is ULIP Insurance for Retirement

If you have to take a free life after retirement, then you have to prepare it very much before retirement, which will change your dreams into reality. It is important that you choose and invest in a Best Retirement Option. These options can be anything like the Mutual Fund, ULIP, etc.

What is ULIP Insurance for Children Education

As you are parents, your biggest responsibility is to educate your children and you want to ensure that your child gets a good education and in any condition, in any of your children’s studies, There can be no obstacles. You also want your child to experience a variety of co-curricular activities like Dancing, Sports, and Painting, etc.

There are many benefits in the ULIP plan that helps you secure your child’s future. In these plans, your child is paid a small amount of money for the main events of his life, so that the future of your child is not bad due to any incident.

What is ULIP Insurance for Wealth Collection

If you want to invest your money and also want to ensure some part of the insurance then you should purchase the ULIP plan because both of these functions are better in ULIP than any other plans.

The main reason for investing in this plan is that your money is deposited for a fixed amount of time and gradually it becomes a large amount. By using this plan, you get the flexibility for your Long-Term Financial Goals that will help you to achieve your future goals such as buying a home, your child’s high education, Personal Car, etc.

NOTE:

ULIP plan is more suitable for those who are over 20 years old but younger than 30 years.

ULIP Insurance Plan Provider in India:

- SBI Life – SBI ULIP plan

- LIC of India – LIC ULIP plan

- Aegon Life

- Canara HSBC

- ICICI Prudential – ICICI ULIP

- Edelweiss Tokyo Life Insurance Reliance Life

- Bajaj Allianz

- HDFC Life ULIP

- Max Life Insurance

- DHFL Pramerica Life Insurance

- Aviva Life Insurance

- Kotak Mahindra Life

Summary:

Unit Linked Insurance Plan (ULIP) is considered a great investment plan in today’s era, with which you also get an option of partial withdrawal in emergencies.

FAQ:

Q. What is the full form of ULIP?

A. Do you know what is the full form of ULIP? It is “Unit Linked Insurance Plan”

Q. Is ULIP a good investment?

A. ULIP (Unit Linked Insurance Plan) is an outstanding investment option and it is very important to carefully understand these ULIP insurance charges before you make any investment in the ULIP insurance plan.

Q. What is ULIP Insurance Plan?

A. Unit Linked Insurance Plan (ULIP) is an option by which you can invest in life insurance and mutual funds simultaneously. Unit Linked Insurance (ULIP) can go for a combination of insurance and investment.

Q. What is the meaning of the ULIP plan in insurance?

A. In insurance, the ULIP plan simply means a long-term investment

Q. How does the ULIP plan work?

A. In the ULIP insurance plan, a small portion of the premium secures life insurance and the rest of the money is invested in mutual funds.

Q. Which ULIP plan is best?

A. There are plenty of insurance companies out there who offers ULIP plans. Among those plans, to find out the best suited ULIP plan check out its features to see whether it fulfills your requirements or not.